- From tariffs to trade wars: How U.S. politics challenges EU agreements - 20 June, 2025

- The Deteriorating Sino-Dutch Relations - 19 May, 2025

- The Problem of Over-tourism in Europe - 13 March, 2025

- Taxing U.S. Big Tech: Europe’s Countermove to Trump’s Tariff Agenda - 27 October, 2025

- From tariffs to trade wars: How U.S. politics challenges EU agreements - 20 June, 2025

- Will Russia Pay for Ukraine’s Reconstruction? Analysing European Regulation on Utilising Extraordinary Net Profits from Frozen Assets - 2 August, 2024

President Donald J. Trump meets with the President of the European Commission Ursula von der Leyen during the 50th Annual World Economic Forum meeting Source: The White House from Washington, DC

Since Donald Trump assumed office as the 47th president of the United States in January, uncertainty has loomed over international trade. Global stock markets have struggled to find a stable footing, while nations grapple with shifting alliances, unsure who remains an ally and who has become an enemy.

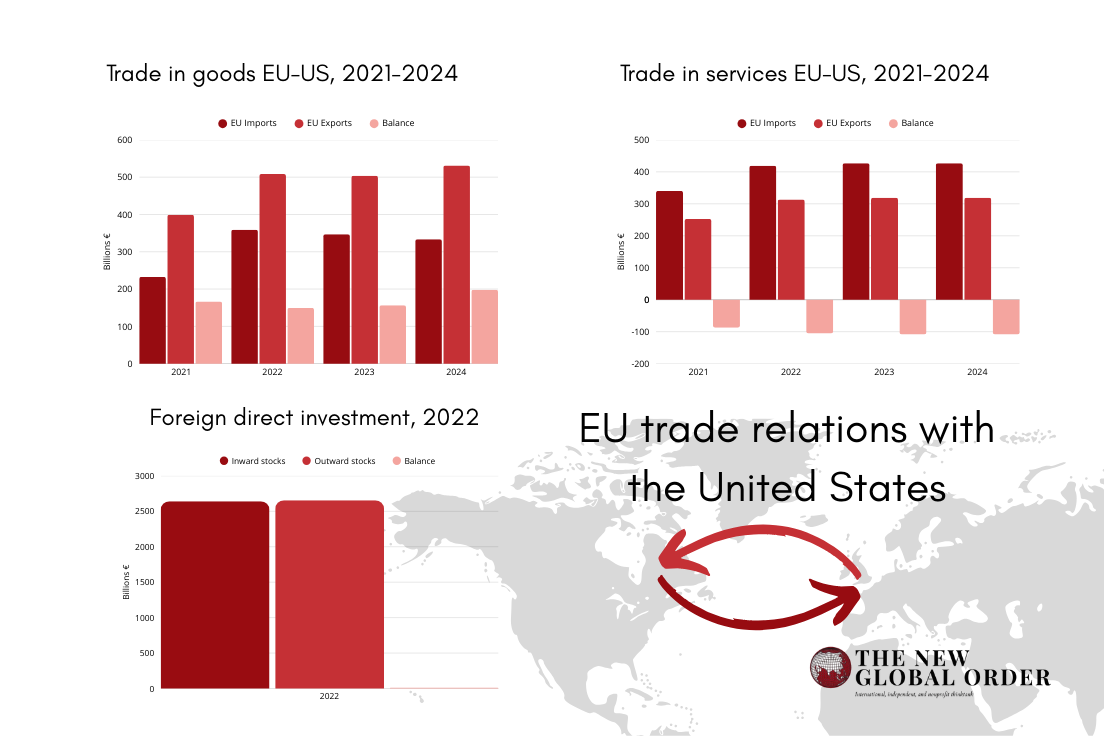

The European Union, which looks to be at the centre of the new executive branch’s dartboard, is no stranger to this situation. It is becoming less and less aligned with Washington, but it cannot ignore the importance of the United States as a strategic partner. They share the world’s largest bilateral trade and investment relationship and form the most integrated economic partnership globally. The European Union and the United States are each other’s largest trading partners (European Commission, 2025).

In 2023, the United States was the second-largest supplier of goods to the European Union, following China. Total bilateral trade in goods between the European Union and the United States reached €851 billion. EU exports to the U.S. amounted to €503 billion, while imports from the U.S. totaled €347 billion, leaving the EU with a trade surplus of €157 billion in goods. The picture is different regarding the trade of services; in 2023, total trade in services between the EU and the U.S. reached €746 billion. The EU exported €319 billion in services to the U.S. and imported €427 billion in return, leading to a trade deficit of €109 billion in services for the EU.

This trade imbalance underscores a relationship of mutual dependence between the two partners. However, President Trump has framed it as unfair treatment toward the United States. In his view, countries running trade surpluses are exploiting America’s openness to their advantage.

Trump’s America First trade policy

According to a survey by the Pew Research Center, during the 2024 US Presidential elections, the economy topped the list of the most pressing concerns of US voters, while 54% of the voters expressed confidence in Donald Trump for handling the issue at hand better than Kamala Harris. One of the primary reasons for this view could be attributed to Trump’s nationalist and protectionist international trade strategies. One of his campaign promises dealt with “rebuilding the greatest economy in history” and providing the US citizens jobs by reshoring plans so that they are no longer dependent on China for manufacturing goods. This was accompanied by Trump’s strategy of applying aggressive tariff measures to serve the dual purpose of gaining a footing in the international trade regime while protecting domestic manufacturers.

As mentioned previously, the EU enjoys a surplus in trade of goods with the US. In comparison to the 2023 data, EU exports increased by 5.5%, while imports declined by 4.0%, fuelling a sense of hostility towards the union. The Trump administration had previously accused the EU of taking undue advantage of its trade agreements. Before his second inauguration, he threatened the EU to reduce the trade surplus it maintained with the US by increasing US imports of oil and gas. The EU responded by stating that the trade surplus of the EU in goods was offset by a trade deficit in services.

In February, after assuming the presidency, keeping in view his policy, Trump hinted at a tariff increase “pretty soon” creating panic in the stock market. On March 12, Trump announced a blanket tariff on all steel and aluminium imports, which included the EU. On April 2, a 20% reciprocal tariff on all EU-imported goods was announced. Nevertheless, shortly after the public statement, the implementation of the tariffs was paused, providing a 90-day buffer for both parties to carry on talks and conduct negotiations. The baseline tax of 10% is, however, still applicable to all EU imports entering the US.

Impact on EU Trade

European companies have faced higher costs and supply chain disruptions, while key EU industries—such as automotive, agriculture, and technology—have been significantly affected by U.S. tariffs. These factors have contributed to growing uncertainty in transatlantic trade relations.

The theory of international trade suggests that with the imposition of a tariff, the imports become expensive for the Home country, benefiting Home producers, while the imports from the Foreign country decrease. Keeping this view in mind, it can be inferred that the direct effect would be reduced eurozone exports to the US.

As the demand for goods made in the EU reduces on account of higher prices in the US consumer market, domestic manufacturers in the US would be advantageous, while EU exporters will have to look for alternatives or narrow down their production. This could be accompanied by an economic downspiral. The main reason for Trump to apply these tariffs is to correct the trade imbalance with the EU, which could indeed lead to a current account deficit in the EU if the EU does not retaliate with counter-tariffs. Such a case can further contract consumption and investment, slowing growth.

The effects of the duties can vary regionally as well as sectorally. Among the leading economies, Germany, France, and Italy are deeply integrated with the US market, varying across sectors. In the automotive sector, tariffs could put 300,000 jobs at risk in Germany, the top exporter of automobiles in extra-EU trade. Other countries such as Austria, Sweden, and the Visegrad countries, particularly Slovakia, would also be profoundly affected. According to the Vienna Institute for Economic Studies, the short-term effects of a 25% duty resulting in an assumed 25% decline in exports would contract EU automotive exports by 0.14% and lead to a GDP reduction by 0.07%. The long-term effects would be reflected in declining real incomes and wages, most prominently in Slovakia by 0.1%, Ireland by 0.06%, and Hungary by 0.04%.

Another sector causing harm to both economies is the agricultural, food, and beverage industry. The proposed 20% taxes would discourage US importers from sourcing wine, spirits, beer, cheese, olive oil, fruits, and vegetables, etc. Within the industry, wine exporters are expected to be the worst affected, which (along with champagne and spirits) recently received a warning of a 200% tariff in March 2025. Marzia Varvaglione, president of the European Committee of Wine Companies (CEEV), expressed her concerns over the dire consequences of the tariffs on the EU’s wine trade, commenting on the absence of an alternative wine market.

The EU, being the largest supplier of luxury goods at 70%, including apparel, jewelry, leather items, watches, perfumes, and cosmetics, amounting to €288 billion in 2024, can also receive a severe blow. The shares of luxury companies LVMH(LVMH.PA) were down by 2% and Kering (PRTP.PA) by 31%, giving a pessimistic outlook for the consumers. The brands primarily located in France and Italy were counting on American consumption to counter the weak demand persisting in China. Brands such as Gucci, Cartier, and Chanel have already hiked their price by 3% to neutralise the effect of the duties, yet the customers may refrain from purchasing due to a global slowdown putting the industry at a standstill.

While the Trump administration has paused the reciprocal tariffs for 90 days, the universal duties on steel and aluminium took effect on 12th March 2025. Previously, during the first Trump administration, the US and the EU engaged in a trade conflict affecting EU steel and aluminium as well as its derivative exports worth €6.4 billion (€8 billion in 2024 trade flow terms) and €40 million respectively before pausing any retaliatory measures until 31st March 2025. During this period, EU exports declined by more than a million tonnes. Now, the newly introduced 25% customs duty is estimated to affect EU exports worth €26 billion.

Moreover, since these restrictions are not limited to the EU but more than 180 other countries, they can lead to an indirect effect on the EU’s internal market. The tariffs can force countries to redirect their products into the EU market, thus making it difficult for domestic producers to compete with the cheaper imports. For instance, the US has levied a 145 percent duty on Chinese imports, leaving analysts worried about China’s strategy to offload the excess. Many retailers are speculating that Chinese manufacturers will flood their products in the EU via platforms such as Temu, Shein, and Amazon.

Taxes on car markers in Canada and Mexico, though paused for the time being, could exacerbate tightly interwoven supply chains with many EU Member States, including Germany, creating short-term inflationary effects, ultimately leading to rising unemployment levels. The interconnectedness of these networks was witnessed by the immediate drop in Germany’s index (DAX) by 0.7% and French automotive supplier Valeo (VLOF.PA) by 7.7% as April 2, the day of the announcement of tariffs, came closer. The pan-European STOXX 600 fell by 1.1%.

Besides, many top EU car manufacturers, including the Volkswagen group, BMW, Mercedes-Benz, Renault, and Stellantis, depend on Mexico for procuring components and setting production processes. The Audi division of the Volkswagen group makes the car models Q5 and Q5 Sportback at its San José Chiapa. Since it does not fulfill the requirement of the 75% local content of the revised United States-Mexico-Canada Agreement (USMCA), they are liable to pay the 25% tax. This will significantly increase the cost of production and subsequently put a burden on the consumers in the form of price hikes.

The sudden surge in customs duties also questions the future of trade policies pursued by the EU. With the US turning towards import-substitution measures, the EU may follow in its footsteps. Given the threats of dumping by Chinese producers, it may urge the EU to impose protectionist policies on it. On the contrary, it may encourage the EU to look for new avenues and diversify its export base. On a three-day visit to Vietnam, Spain’s Prime Minister Pedro Sánchez, stressing the importance of free trade, insisted that Europe look towards Southeast Asia for opening their markets for one another.

EU Responses: Retaliatory Measures and Trade Diversification

The European Union has reaffirmed its commitment to engaging with the United States through an open, collaborative, and constructive dialogue. This is illustrated by the travel of the EU trade commissioner Maroš Šefčovič to hold meetings with US Commerce Secretary Howard Lutnick and US Trade Representative Jamieson Greer (Euronews, April 11th, 2025). After weeks of deadlock, the Commission is hoping to advance negotiations on tariffs. In parallel to the negotiations, the EU continues to design countermeasures to the Trump administration’s new trade measures. In addition, Brussels is exercising “strategic patience” while, in light of recent developments, deepening ties with other global partners, including the Mercosur bloc, and potentially even China.

Legal framework for the EU response

The European Union’s first line of defense is the Enforcement Regulation (Regulation 654/2014), which allows the bloc to impose so-called rebalancing measures in response to various trade disputes, including cases where a foreign country introduces safeguard measures to counter a sudden import surge. This was invoked when the first Trump administration imposed global 25% steel and 10% aluminium tariffs.

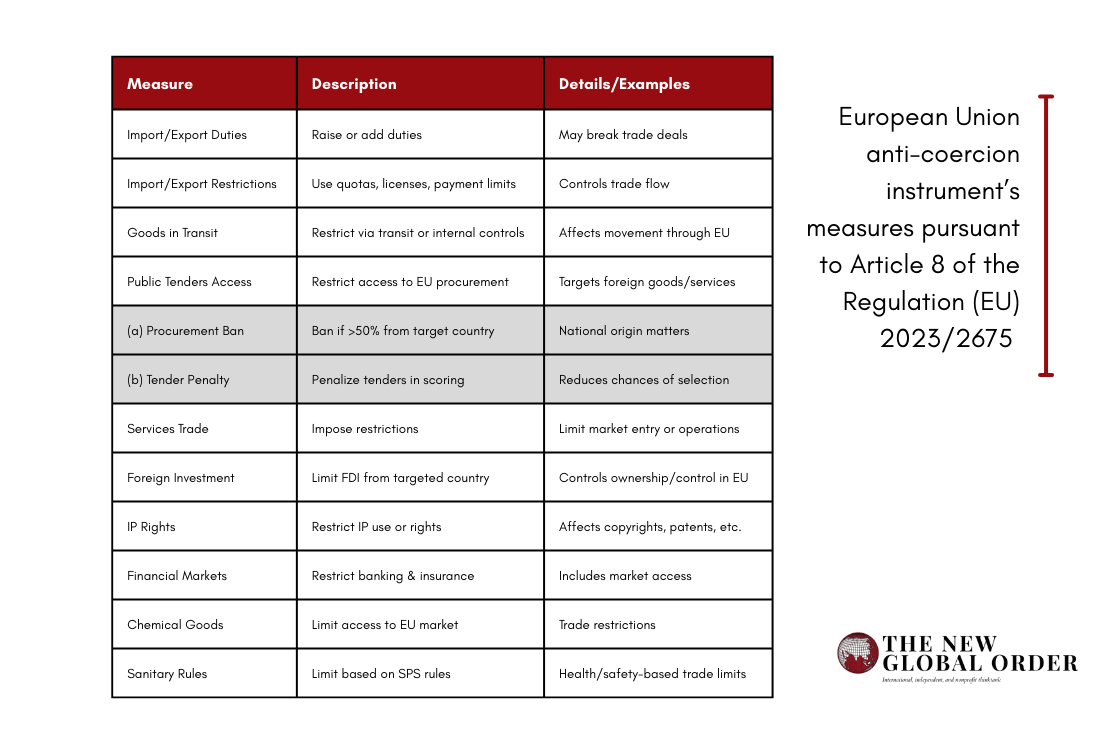

In addition, the European Commission could activate the anti-coercion instrument (ACI) (Regulation 2023/2675). It provides the EU with the means to deter and respond to economic coercion, and thereby better defend its interests and those of its Member States on the global stage. This instrument was adopted when the EU realised that it was difficult to respond quickly and effectively to tariff threats by the first Trump administration (Freshfields, April 8th, 2025). It gives the EU a wide range of possible countermeasures when a country refuses to remove the coercion.

European reactions. The strategic calm: He who laughs last, laughs longest?

The first European reaction was on 12th March 2025, where the Commission informed about the launch of two countermeasures against the steel and aluminium tariffs: the reimposition of the suspended 2018 and 2020 rebalancing measures; and the imposition of a new package of additional measures (European Commission, March 12th, 2025).

After the mandatory period of consultation, the President of the European Commission announced on April 3rd that a first package of countermeasures in response to tariffs on steel and aluminium imposed by Donald Trump on February 10th was already finalising (European Commission, April 3rd, 2025). These measures were announced on April 9th when EU Member States voted in favour of the European Commission’s proposal to introduce trade countermeasures against the United States. The duties will start being collected as of 15th April (European Commission, April 9th, 2025).

However, the list was trimmed after the EU executive, facing pressure from member states, backed down and removed bourbon, wine, and dairy products. The move followed President Trump’s threat to impose a 200% retaliatory tariff on European alcoholic beverages (Reuters, April 7th, 2025).

In addition to the tariffs on aluminium and steel, tariffs on automotive parts are expected on 3rd May 2025. The EU has yet to respond to Trump’s 25% tariff on cars or the forthcoming U.S. tariffs on pharmaceuticals. In the meantime, negotiations are there, and Europe has offered the U.S. “zero-for-zero” tariffs on cars and other industrial goods. The European bloc considers that this offer could be very beneficial for the American car industry.

These measures marked only the beginning of the storm. European retaliation extended beyond President Trump’s imposition of 20% “reciprocal” tariffs on all EU exports. When the so-called “Trump’s Liberation Day tariffs” were announced, the European Union appeared poised and prepared. However, as of April 9th, those tariffs have been put on pause. President Trump announced a temporary suspension of tariffs above 10% for most U.S. trading partners (Politico, April 9th, 2025).

Still, the EU has made it clear: the toolbox is open, and with the unpredictability of the Trump administration, there’s little room for complacency. The measures announced so far are just the beginning; more remain on the table. Among them, the prospect of taxing large U.S. tech companies remains firmly under consideration (The Economist, April 9th, 2025).

Finding “new” trade partnerships

Europe remains committed to diversifying its trade partnerships, engaging with countries that represent 87% of global trade and share its values of free and open exchange of goods, services, and ideas (European Commission, April 10th, 2025). But the key question remains: who could replace the United States as Europe’s primary partner?

Some European leaders advocate for distancing from Washington and strengthening ties with other global players. Others, however, argue that staying close to the U.S. remains essential (Politico, April 11st, 2025).

Latin America, and particularly the Mercosur countries, appears to be at the top of the EU’s list for trade diversification. The EU has been stepping up dialogue with the region for several years now, aiming to strengthen strategic autonomy and reduce dependency on traditional partners.

Over the past two years, the EU has updated its trade agreements with both Mexico and Chile. More notably, it has reached a major new agreement with Mercosur. If ratified, the EU-Mercosur deal would establish a free trade area encompassing over 770 million people, representing a quarter of global GDP. The agreement is expected to significantly boost trade between the two regions, already closely linked economically. According to studies by the Bank of Spain, trade could increase by more than one-third in the long run.

While the agreement has faced considerable resistance, shifting global dynamics have changed the conversation. After the U.S. raised tariffs and intensified its trade war stance, countries like Finland and Sweden voiced their support for the EU-Mercosur deal, seeing it as a timely opportunity to reinforce global trade ties (AFP, April 8th, 2025).

Another notable case is the evolving relationship between the European Union and China. Could this be a classic enemies-to-lovers scenario? The EU and China have had trade disputes in the past over various products, such as electric vehicles. However, it suggests that the enemy of my enemy is my friend. United in adversity, there seems to be a willingness to strengthen ties between the two. The visit of Spain’s PM Pedro Sanchez, has helped to see this vision. Both consider that they have to jointly safeguard the trend of economic globalisation and a fair international trading environment, and jointly resist unilateral and intimidatory practices.

Sources report that EU leaders plan to meet Xi Jinping in China in July. The last such summit was held in Beijing in 2023 and, according to protocol, the next edition should be held in Brussels. The EU’s willingness to host China again suggests that European leaders are eager to please the Chinese president and use the summit, which coincides with the 50th anniversary of the establishment of EU-China relations, to forge stronger ties with China (Politico, April 11th, 2025).

Conclusion

Recent events have shaken nations and heightened market insecurity. However, the European Union is making a virtue of necessity. Its traditional slow pace, bureaucracy, and requirement for consensus have paradoxically provided the stability and reliability so crucial amid the shifting sands the U.S. executive seems intent on stirring up.

“Old Europe” now has a chance to reject protectionism and position itself as the world’s leading advocate for free trade. As Ursula von der Leyen stated on April 3rd, “Europe has everything it needs to make it through this storm” (European Commission, April 3rd, 2025). But what exactly was she referring to? A strong legal framework? New trade partnerships? An unshakable calm and a commitment to negotiation?

What are Europe’s aces up its sleeve?

For further thought:

- Would the EU be able to reverse the emerging trend of protectionist trade policies?

- What do you think the EU’s response should be?

- Do you think that, in the long term, strengthening relations with China will be dangerous for European trade?

Suggested readings:

- Brattberg, Erik, Pastorelli, Jacopo, and Schwab, Benjamin (2025) The EU could respond to Trump’s tariffs with a new ‘anti-coercion instrument.’ Here’s what to know, Atlantic Council.

- Pettis, Michael, and Hogan, Erica (2024) Trade Intervention for Freer Trade, Carnegie Endowment for International Peace.

- McKibbin, Warwick J., and Noland, Marcus (2025) Modelling a US-EU trade war: Tariffs won’t improve US global trade balance, Peterson Institute for International Economics.

.jpg){kind=link}